Retirement Tools and Calculators

| Investing for Retirement | Nearing Retirement | Living in Retirement |

Congratulations. You're here because you know the person that matters most in your retirement planning is you. And no matter what stage you're in – early in your career, actively contemplating retirement or already retired – we're here to help.

Use these resources and tools to learn more about the risks and concerns you'll face – as well as the opportunities – as you make your retirement plans. Simply click on the button above that best represents where you are in your retirement planning process and follow the steps.

Benefits of starting early

Compounding Interest

The main benefit of starting early is to take advantage of compounding interest. Compounding interest allows you to earn interest on both the principal you invest and the interest you earn – potentially enabling you to turn a small sum into a substantial one over time.

![]() It's important to understand how building up your assets now will help you cover your expenses and achieve your goals in retirement. Learn more...

It's important to understand how building up your assets now will help you cover your expenses and achieve your goals in retirement. Learn more...

When saving for retirement, or another future goal, consider using dollar-cost averaging as a strategy - the process of making regular investments on an ongoing basis, regardless of price; for example, buy 100 shares of an investment each month, quarter or year. You are aiming to buy more shares of a security when its share price is low, and fewer shares when its price is high. Over time, it’s likely the average cost per share will be lower than the average market price. For many, this is the most realistic way to save toward retirement because these periodic investments come from paycheck as opposed to having a lump-sum of money to invest all at once.

Dollar-cost averaging cannot guarantee a profit or protect against a loss, and you should consider your financial ability to continue purchases through periods of low price levels. The example provided is hypothetical and given for illustrative purposes only. It does not represent an actual investment.

Managing Risk

Diversification is key to managing risks

At this stage in life, you may discover you are better positioned to withstand short-term market fluctuations than someone nearing or in retirement. We can work with you to identify the risks most relevant to your situation, as well as to determine the appropriate allocation of assets to balance these risks, which may include:

Market |

Fluctuation or volatility in the performance of financial markets. How and where your assets are allocated across different asset classes plays a key role in managing market risk. |

Inflation |

Costs of goods and services increase over time. Your cost of living at retirement might be higher than it is now, as inflation erodes the value of your savings and reduces your purchasing power over time. |

Longevity |

Longer life expectancies mean the assets you save toward retirement will need to last longer. As you determine your savings goals, consider you may need your assets to generate income throughout a 20- to 30- year retirement. |

Diversifying your savings among several asset types may enable you to take advantage of growth potential in different sectors and various financial markets. You may want to avoid placing your retirement savings in one type of asset, so to balance performance in times of market fluctuation. Also consider dollar-cost averaging which is the process of making regular investments on an ongoing basis, regardless of price. This can make the average cost of your investments lower than the average market price over time. Although dollar-cost averaging may not mitigate market, inflation, and longevity risks, it typically offsets their impact on the value of your investments.

Contact us for more information on how we can work together to manage these risks by applying a comprehensive process to plan for your retirement.

Diversification and Dollar cost averaging do not assure a profit and does not protect against loss. Dollar cost averaging involves continuous investment regardless of fluctuating price levels of such securities. Investors should consider their financial ability to continue purchases through periods of low price levels.

Managing Life Changes

Whether you’re changing careers, buying a new house or starting a family, we can help you live the life you choose today, while still prudently planning for the future.

Wherever your work or life leads you, we can assist you in managing your cash flow and allocating your resources, helping you reach both your short- and intermediate-term goals without endangering your long-term plans.

Please contact us so we help you determine an appropriate course of action for your retirement plan.

|

If you're planning to buy a new home, we can help you allocate an appropriate portion of your holdings to investments designed to facilitate that purchase. We can also assist with managing the funds needed for your changing lifestyle, including mortgage, property taxes and related expenses. |

|

If you’ve recently started a family – or are contemplating doing so – we can help you optimize your investments, meet the expenses you will incur over the next several years and help make sure your life goals are achievable and realistic. |

|

As you change employers – or go to work for yourself – you typically have several options for dealing with the funds you’ve accumulated in your former employer’s retirement plan, such as a 401(k) or 403(b). The option you choose could have significant tax implications or alter your existing retirement plan. |

Making a Plan

At this stage in your life, your goal should be to begin building up enough assets to provide adequate income to meet your needs throughout retirement – accounting for factors like increased longevity, healthcare costs and inflation. To accomplish this goal, you need a plan.

How Much Money Will You Need?

To maintain your standard of living, a general rule of thumb suggests your annual retirement income should equal approximately 80% of your income the year you retire. So, if you determine you'll earn $100,000 the year you retire, you'll need to save enough to provide $80,000 per each year you are retired.

![]() It's important to think through how much income you'll need to cover your expenses and achieve your goals in retirement. Learn more

It's important to think through how much income you'll need to cover your expenses and achieve your goals in retirement. Learn more

Once you've evaluated your income needs for retirement, it's time to develop a well-crafted retirement plan. We can help guide you through this often complex process, which can involve different strategies, each with possible tax deferred advantages. These strategies may include:

- Contribute to your employer's retirement plan, such as a 401(k) or 403(b), and take advantage of match programs; consider automatic payroll deduction for dollar cost averaging. Or roll over assets from a previous employer's plan.

- If you don't have an employer plan, or if you wish to invest separately from your employer sponsored plan, consider investing regularly using an Individual Retirement Account (IRA). You may wish to discuss the tax implications of both traditional and Roth IRAs to determine which best meets your needs.

Traditional IRA |

You may be able to deduct the contribution from your income taxes, depending on participation in a workplace plan and income. |

Roth IRA |

You do not receive the income tax deduction. But, when you reach retirement age, you are able to take qualified withdrawals tax-free.* |

Simple And |

There are other tax-deferred retirement saving options to consider if you are self employed or a small business owner |

*Unless certain criteria are met, Roth IRA owners must be 59½ or older and have held the IRA for five years before tax-free withdrawals are permitted.

You should discuss any tax or legal matters with the appropriate professional.

In an IRA, Investment-related expenses may include sales loads, commissions, the expenses of any mutual funds in which assets are invested and investment advisory fees. We can review all of the allowed options, such as keeping your 401(K) at your former employer, rolling it to your new employer, moving it to your own IRA or taking a distribution. Each option has potential benefits and drawbacks, so we'll help educate you based on your individual situation.

Assessing Your Current Situation

Do you know how much income you need your assets to generate once you retire?

Chances are you should reevaluate your retirement plan. Your financial circumstances, personal situation or retirement goals may have changed since the last time you reviewed your plan. Market turbulence may also have adversely affected your portfolio, making a fresh look important.

As you revisit your plan with us, we will take a look at factors such as:

- Your income sources

- Your assets and anticipated expenses

- The rate at which you’ll be able to spend in retirement

You’ll also want to consider what appropriate adjustments may entail for you, for example:

- Paring non-essential spending

- Reallocating your investment assets

- Reevaluate your retirement priorities and discuss tradeoffs

Contact us for help with reviewing your retirement plan and making the necessary adjustments to put you on the path to a comfortable retirement.

There is no assurance that any investment strategy will be successful. Investing involves risk and investors may incur a profit or a loss. Past performance is not indicative of future results.

![]() It's very important to ensure that your assets are on target to generate the income you'll need to cover your expenses and achieve your goals in retirement. Learn more...

It's very important to ensure that your assets are on target to generate the income you'll need to cover your expenses and achieve your goals in retirement. Learn more...

It's time to get started. Accurately determining the income your investments can generate and building in a buffer to preserve your retirement under difficult conditions takes considerable time and work.

Part of building a retirement plan is articulating your priorities and goals for life in retirement. By working with us, we'll identify these factors and discuss others that play a key role in a successful retirement plan, such as:

- Your income sources

- Your assets and anticipated expenses

- The rate at which you'll be able to spend in retirement

Having a plan and continuing to adjust it over time can help put you on the path to a comfortable retirement. Please contact us to get started on formulating a plan to help meet your specific goals and objectives.

There is no assurance that any investment strategy will be successful. Investing involves risk and investors may incur a profit or a loss. Past performance is not indicative of future results.

![]() It's very important to ensure that your assets are on target to generate the income you'll need to cover your expenses and achieve your goals in retirement. Learn more...

It's very important to ensure that your assets are on target to generate the income you'll need to cover your expenses and achieve your goals in retirement. Learn more...

Making a Plan

First, make sure your retirement team is in place, starting with your financial advisor. Depending on your situation, we may also act as your team's "quarterback," coordinating and working with family members, your CPA, an estate attorney, and insurance and trust professionals.

Next, establish your priorities. We can assist you in understanding factors that will impact your retirement plan, such as your retirement lifestyle, risk tolerance, retirement date, unknown risks and your desire to support your family members or a favorite charity.

You must also have a thorough understanding of your situation. We can assist in putting your retirement into perspective by taking a financial inventory, which includes identifying your income sources and assets and distinguishing between your needs and wants.

Legacy Planning

You may want to fund a comfortable retirement, while still allocating funds to leave an inheritance for family or donate to a charity. But your first priority should be to ensure your expenses can be met before you leave a monetary legacy behind.

We can assist with estate and legacy planning, including helping to optimize your assets, potentially mitigate tax implications, and determine the course most appropriate to your situation. We can also help select effective vehicles to implement your plans.

Evaluating Your Retirement Income

Although many individuals nearing retirement have at least one 401(k), IRA or defined benefit plan, rarely will those income sources meet the full range of retirement expenses.

By working with us, we can help determine how much you will need to withdraw from your retirement portfolio to live comfortably in retirement. The less you withdraw, the better your chance your assets can generate income through the duration of your retirement. The general rule of thumb is a maximum withdrawal of 4% to 6% per year, but you may need to withdraw more or less depending on your specific circumstances.

You may need to adjust your rate of withdrawal based on future market performance. The sustainable rate of withdrawal is historical and will fluctuate. If your rate of withdrawal is greater than the growth of your assets, you may exhaust your principal.

![]() It's important to know how you'll finance your needs and wants in retirement. Learn more...

It's important to know how you'll finance your needs and wants in retirement. Learn more...

Social Security benefits are another important aspect of your retirement plan. A variety of factors, such as your age, spouse's earnings and other sources of income, can affect when you may need to begin receiving your benefits.

Contact us to gain the insight you need to help determine the most appropriate course for you.

Planning for Social Security

Most Americans consider Social Security benefits to be a significant source of reliable income in retirement. Deciding how and when to start drawing benefits will have a significant impact on your income, and thus your lifestyle in retirement, so it’s especially important to understand the options available to you.

The decision around when to begin taking Social Security is a key factor – but there are other important factors to consider:

- Your health and life expectancy

- Your spouse's or ex-spouse's benefit

- Whether or not you plan to work after age 62

- Your taxable income or other income sources in retirement

Contact us to take the first step toward understanding when and how to apply for benefits.

Managing Risk

Regardless of your age or your financial situation, every investment decision entails some sort of risk. We will work with you to identify the factors and risks most relevant to your situation and plan for them, including:

Longevity |

Longer life expectancy means your assets have to last longer. You have to consider the possibility of living 20 or 30 years after you retire. |

Inflation |

For example, health insurance premiums and prescription costs are rapidly increasing. If you are retired, this would increase your cost of living, erode the value of your savings and reduce your purchasing power. |

Spending and Withdrawals |

Overspending, living beyond your means or withdrawing more than the recommended percentage from your retirement funds can adversely affect how long your assets last. |

Market Risks |

Market declines and the timing of these declines pose risks. How and where your assets are allocated across different asset classes plays a key role in managing this risk. |

Unknown Risks |

Major health events, disability, long-term care needs and other unexpected occurrences can complicate a retirement plan. |

Contact us for more information on how we'll work together to help address these risks by applying a comprehensive process to plan your retirement.

Healthcare Considerations

It’s never too early to start thinking and planning for retirement, especially when it comes to major expenses like healthcare. For one thing, Americans are living longer. Yes, increased longevity is wonderful, but it also comes with a greater risk of experiencing changes in health, which could mean greater expenses as healthcare costs rise. The fact is, even with insurance and Medicare, out-of-pocket healthcare costs in retirement can be expensive, with the potential to derail even the best-laid plans. Understanding potential costs, evaluating your options and developing a comprehensive plan that accounts for those expenses can help you achieve a secure, comfortable retirement.

Costs to take into consideration:

- Medicare premiums, deductibles and copays

- Supplemental coverage costs

- Prescription copays

- Hearing, dental and vision costs

- Long-term care insurance

- Other out-of-pocket expenses

![]() Learn more about retirement income planning and how healthcare expenses factor into your overall plan.

Learn more about retirement income planning and how healthcare expenses factor into your overall plan.

Business Succession

If you’re a small business owner and haven’t already determined your exit strategy, don’t wait any longer. Among many other decisions, you’ll need to determine the most appropriate structure for divesting your business and tapping into the value it represents.

![]() Consider how your business may be an important asset to fund your retirement plan now or in the future. Learn more …

Consider how your business may be an important asset to fund your retirement plan now or in the future. Learn more …

The checklist below shows some of the key options you could consider when thinking through this part of your planning:

|

|

Positioning yourself to reap the benefits of the work, time and effort you’ve put into your business requires time, thought and skill. Feel free to contact us to discuss in more depth how these options may fit into your specific situation.

There is no assurance that any investment strategy will be successful. Investing involves risk and investors may incur a profit or a loss. Past performance is not indicative of future results.

Please note, changes in tax laws or regulations may occur at any time and could substantially impact your situation. While we are familiar with the tax provisions of the issues presented herein, as financial advisors of Raymond James we are not qualified to render advice on tax or legal matters. You should discuss any tax or legal matters with the appropriate professional.

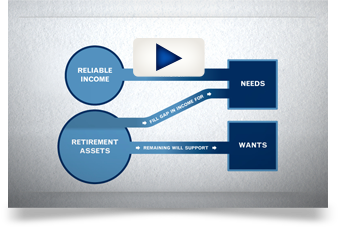

Give Your Plan a Checkup

Once you’ve retired, managing your money is more important than ever. During your retirement years, your personal goals and situation — as well as the economic environment — are likely to shift. These changes require careful scrutiny, perhaps resulting in adjustments related to your goals, your portfolio or both. The video below can assist in visualizing how your income sources and retirement assets fund your needs and wants in retirement.

We can work with you to regularly review and reassess your portfolio to give you confidence that your portfolio is appropriately balanced between growth-oriented investments and income-focused assets. Contact us today.

Healthcare Considerations

Many retirees underestimate how much they’ll need to cover healthcare expenses. In fact, a Center for Retirement Research study recently estimated out-of-pocket costs for a healthy 65-year-old couple to be $260,000 to $570,000 for their entire retirement. Income from investments and Social Security can go toward paying ongoing medical costs, such as Medicare premiums, deductibles and copays, but as healthcare costs continue to rise, this could place a significant strain on your retirement. We can work together to anticipate your healthcare expenses in retirement and account for them within your overall retirement income plan.

Another risk-management option is long-term care insurance, which covers a range of nursing, social and rehabilitative services for people who need ongoing assistance due to a chronic illness or disability. While you can’t know for sure if you’ll need long-term care or for how long, a comprehensive policy can help you plan for the unexpected.

Some people choose a policy to help:

- Protect assets

- Add options for quality care

- Relieve family and friends from the stress of providing care

- Preserve their independence, dignity and financial freedom

![]() Learn more about retirement income planning and how healthcare expenses factor into your overall plan.

Learn more about retirement income planning and how healthcare expenses factor into your overall plan.

Legacy Planning

Depending on your financial situation, you may be confident you can fund a comfortable retirement and still allocate funds to leave an inheritance for family members or to donate to a favorite charity. The first priority should be ensuring your expenses can be met before you leave a monetary legacy behind.

We can assist you with your estate and legacy planning, including helping you to optimize your assets, potentially mitigate tax implications, and determine the course most appropriate to your situation. In addition, we can help you select effective vehicles to implement your plans.

Keep in mind that money isn't everything. Passing on ideals, such as ethics, morals, faith and religious beliefs, is 10 times more important to both baby boomers and their parents than the financial aspects of inheritance, according to the 2006 Allianz American Legacies Study.

Contact us to learn how we can help you to optimize your assets, potentially mitigate tax implications, and determine the course most appropriate to your situation, including the selection of effective vehicles to implement your plans.

There is no assurance that any investment strategy will be successful. Investing involves risk and investors may incur a profit or a loss. Past performance is not indicative of future results.

Please note, changes in tax laws or regulations may occur at any time and could substantially impact your situation. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of Raymond James we are not qualified to render advice on tax or legal matters. You should discuss any tax or legal matters with the appropriate professional.

Withdrawals and Tax Implications

In addition to Social Security benefits, you probably have at least one IRA, 401(k), pension plan or other assets you're relying on now for income – or counting on later – to finance your retirement years. At this stage we feel that you should work with a professional to maximize the benefits you receive from any withdrawals you are making or plan to make.

![]() Consider how much you need to withdraw from your assets to maintain a sustainable income flow during retirement. Learn more …

Consider how much you need to withdraw from your assets to maintain a sustainable income flow during retirement. Learn more …

Below are some common retirement investments and key considerations for withdrawing your money:

Investments |

Considerations* |

|---|---|

| Taxable Accounts | (i.e., brokerage, savings and checking accounts) |

| Tax-Free/Tax-Deferred Plans | (i.e., Tax-Free – Roth IRA; Tax-Deferred – traditional IRA) |

| Social Security Benefits | The longer you wait to tap these funds, the larger your monthly benefit will be when you do decide to take it. You are required to begin taking benefits at age 70.

|

We can help develop a withdrawal strategy that takes all of these considerations into account. Contact us today.

* Investors should consult with a tax advisor to determine the tax implications of the withdrawal strategies.

There is no assurance that any investment strategy will be successful. Investing involves risk and investors may incur a profit or a loss. Past performance is not indicative of future results.

Please note, changes in tax laws or regulations may occur at any time and could substantially impact your situation. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of Raymond James we are not qualified to render advice on tax or legal matters. You should discuss any tax or legal matters with the appropriate professional.

Tapping Social Security

Although you’re entitled to draw Social Security benefits as early as age 62, tapping into your benefits before full retirement age can permanently reduce your benefits. In general, electing to delay your benefits past full retirement age – up to age 70 – will increase the amount you are eligible to receive.

When to start taking Social Security benefits depends in large part on your income needs and your health. It’s also important to consider how the amount of your monthly benefit might affect your overall retirement plan, including implications for withdrawal rates and your tax situation, among other factors.

Contact us so we can help you choose the strategy most appropriate for you.

Coping With the Unexpected

Widespread economic weakness and market fluctuations have taken a toll on many investors. If you are at all concerned your retirement plan may no longer be sufficient to meet your needs, don't delay taking action. While there are no magic fixes, a number of effective strategies do exist for potentially mitigating losses, generating additional income and planning for growth, including:

- Planning for long-term care needs not covered by Medicare or other insurance

- Paring your spending and rethinking non-essential goals

- Allocating a portion — or a greater portion — of your portfolio to undervalued, growth-oriented investments

- Preserving income with financial products, such as annuities1

- Hedging income against rising inflation with investment options that adjust to changes in the inflation rate, such as Treasury Inflation-Protected Securities (TIPS)2

- Returning to work on either a full-time or part-time basis

We can help you look at your retirement plan comprehensively, determine if you have any gaps, and help you identify ways to potentially minimize losses in order to stay on track in retirement. Contact us today to get started.

Note: Growth-oriented investments generally involve greater risks and may not be appropriate for every investor.

There is no assurance that any investment strategy will be successful. Investing involves risk and investors may incur a profit or a loss. Past performance is not indicative of future results.

Please note, changes in tax laws or regulations may occur at any time and could substantially impact your situation. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of Raymond James we are not qualified to render advice on tax or legal matters. You should discuss any tax or legal matters with the appropriate professional.

1Guarantees are based on the claims-paying ability of the issuing company.

2The principal increases with inflation and decreases with deflation, as measured by the Consumer Price Index. At maturity you are paid the adjusted principal or original principal, whichever is greater. Increases in TIPS principal value as a result of inflation adjustments are taxed as capital gains in the year they occur, even though these increases are not realized until the TIPS are sold or mature. Conversely, decreases in the principal amount due to deflation can be used to offset taxable interest income.

These calculators are hypothetical examples used for illustrative purposes and do not represent the performance of any specific investment or product. Rates of return will vary over time, particularly for long-term investments. Investments offering the potential for higher rates of return involve a higher degree of risk of loss. Actual results will vary.

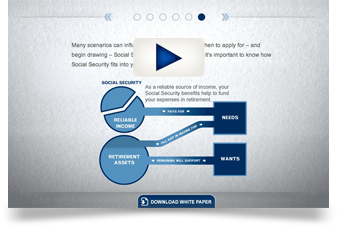

In our disciplined approach, we assist you in visualizing, and understanding, how your income sources and retirement assets will fund your needs and wants in retirement. Key considerations we will evaluate include:

- What are the basics you need during retirement?

- What do you want to enjoy during retirement?

- What income sources are available to pay for expenses during retirement?

- What retirement assets do you have, or might have down the road, to fund your retirement?

Watch the video below for an introduction to the key components of our approach to helping you evaluate retirement. At the end of the video, take advantage of options to learn more, such as exploring the elements of your retirement picture, or taking a financial inventory.

Contact us to take an important first step in your retirement income planning process.